While the pause in interest rates has come as a relief to many, everyone from first home buyers to owner occupiers and seasoned investors faces the prospect of harder times before they get easier.

There is a palpable sense of relief among borrowers that interest rates have been paused for a few months and may even be on their way down in the not-too-distant future.

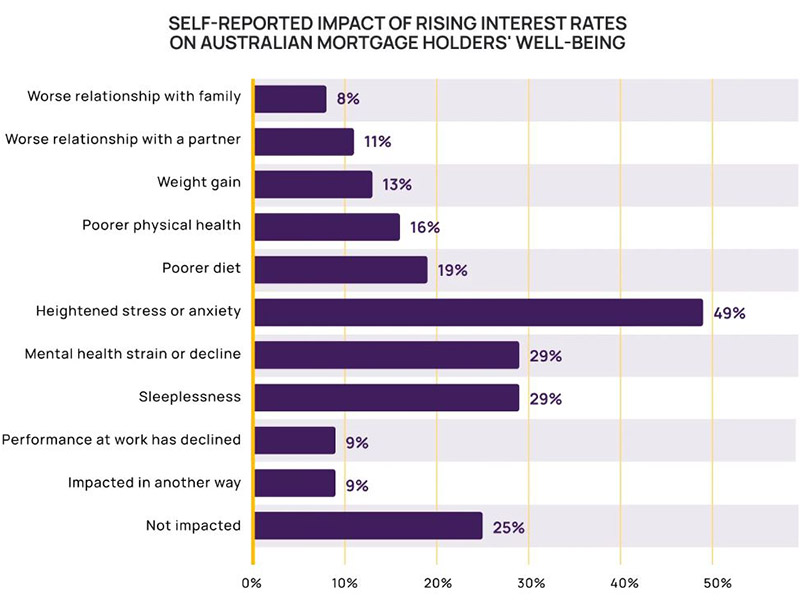

But the reality is that many Australians are feeling the mental, physical and financial strain of a dozen rate hikes since May last year and are struggling to cope with the markedly higher mortgage repayments.

Research conducted by finance platform MNY found that three quarters of Australian mortgage holders have been adversely impacted in terms of their personal lives or wellbeing.

That same 75 per cent said they would not trust any Reserve Bank of Australia (RBA) interest rates forecasts again.

With mortgage interest now averaging around 6.5 per cent, the reign of interest rate hikes means households with a $500,000 mortgage on a variable rate have seen their repayments increase by $1,500 per month in the midst of a cost-of-living crisis as their incomes are eaten away by high inflation.

Source: MNY.

Compounding the situation for those struggling is the argument that interest rates will likely rise, at least once more, before the tide turns and they begin to retreat.

Inflation is on a downward trajectory, which should bring rates down with it, but there some leading indicators that the battle against inflation may not be over.

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist, AMP Investments, said the risk in the short term is still on the upside for rates.

“In the short term, the risks are still skewed to a further increase in interest rates and or a delay in the start of rate cuts as: inflation is still too high; the labour market remains tight with upwards risks to wages flowing from higher minimum and award wage rises; productivity growth is very weak; and the rebound in home prices is partly offsetting the tightening impact of higher interest rates.

“Consistent with this, the RBA retained its guidance that some further rate hikes may be required.

“Key to watch will be the global economy, household spending, inflation and the labour market.”

Mortgage Stress Rampant

While the RBA has consistently stressed that Australians are well placed to manage higher interest rates after accumulating savings during Covid and paying down debt ahead of time.

But researchers are also revealing that mortgage stress is rampant.

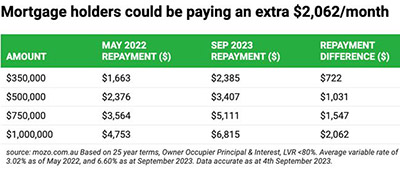

Almost half (46 per cent) of mortgage holders are now under serious financial stress, according to Mozo, as home loan variable rates starting with 5, 6 and 7 become the norm.

The average variable rate of an owner occupier home loan is now 6.60 per cent across all lenders, and 7.21 per cent across the Big Four banks.

Based on the average variable rate of 6.6 per cent, since May 2022 monthly repayments on a $500,000 home loan have increased by $1,031.

In a market where one in three borrowers think refinancing is too much of a hassle, Helen Avis, Director of Finance at Specialist Mortgage, said it was imperative those with stretched finances sought financial advice and better deals.

“The refinancing process may seem time-consuming but the savings on offer make it worthwhile and the application process these days is not as onerous as people may actually think.”

The incentive to refinance is also backed up by research from RateCity.com.au that reveals more than a quarter of Australians (27 per cent) are living payday to payday.

It found one third (33 per cent) of respondents were feeling stressed or uneasy about their budget, while 32 per cent couldn’t survive off their savings for more than a month if they were to lose their job.

Financial strain doesn’t just hit the hip pocket. The survey also found of those in a relationship, over a third (39 per cent) said cost of living concerns have caused increased friction with their partner about money.

First Home Buyers Facing Major Hurdles

First home buyers are being kept out the property market, often as a result of policies that had been intended to help them.

University researchers enlisted by the Australian Housing and Urban Research Institute (AHURI) found that the path to buying a first home is increasingly reliant on parental resources.

Professor Stephen Whelan, University of Sydney, said the issues confronting first home buyers were more complex than just higher property prices.

“While high and rising house prices are often cited as the biggest challenge faced by first homebuyers, our inquiry highlights that the problem is significantly more complex,” Professor Whelan said.

“Critically, we found existing policy settings are likely to have exacerbated rather than alleviated the challenge faced by first homebuyers to finance home ownership.

“Politically seductive measures such as first homeowner grants and tax concessions have failed to arrest declining rates of home ownership over time.”

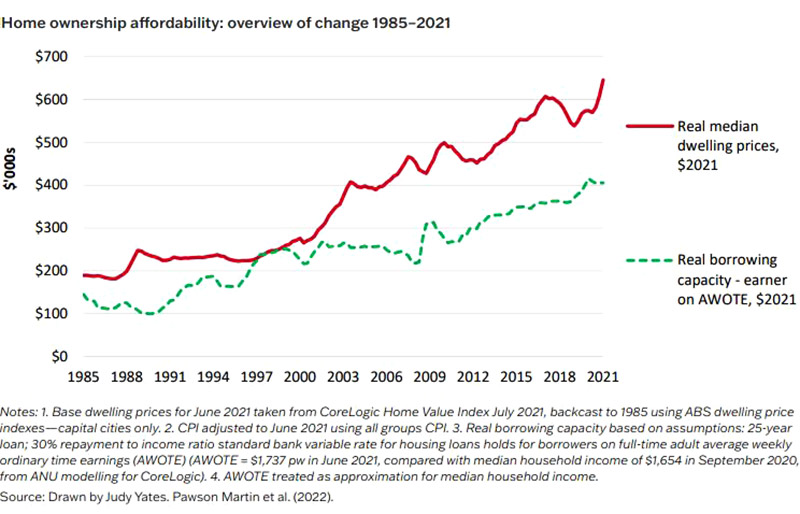

A rapid expansion of owner-occupation in the early postwar period peaked at over 70 per cent in the late 1960s but was followed by a gradually declining home-ownership rate since 2000—especially among younger adults, where the rate for the 25–34 age cohort fell from 51 per cent in 2001 to 44 per cent in 2021.

There is evidence that housing affordability has decreased over time.

AHURI’s research showed that since 2001, the national ratio of median house price to median income has almost doubled to 8.5, and the time required for the accumulation of a deposit for a typical property has increased from six years median earnings in 1994 to 14 years today.

The decline in home ownership among younger adult cohorts has occurred despite expenditures in excess of $37 billion over five decades designed to enable first home ownership.

AHURI’s findings stated that policies designed to assist first home buyers must recognise and address structural issues associated with the treatment of housing in the tax and transfer system.

“Policy settings need to encompass intermediate tenures, such as shared equity as legitimate housing outcomes that may enable households to attain homeownership,” the report said.

Article Q&A

What percentage of borrowers are in mortgage stress?

Almost half (46 per cent) of mortgage holders are now under serious financial stress, according to Mozo, as home loan variable rates starting with 5, 6 and 7 become the norm. Research conducted by finance platform MNY found that three quarters of Australian mortgage holders have been adversely impacted in terms of their personal lives or wellbeing.

Will interest rates rise or fall?

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist, AMP Investments, said the risk in the short term is still on the upside for rates, before easing in mid to late 2024.