While the pause in interest rates has come as a relief to many, everyone from first home buyers to owner occupiers and seasoned investors faces the prospect of harder times before they get easier.

There is a palpable sense of relief among borrowers that interest rates have been paused for a few months and may even be on their way down in the not-too-distant future.

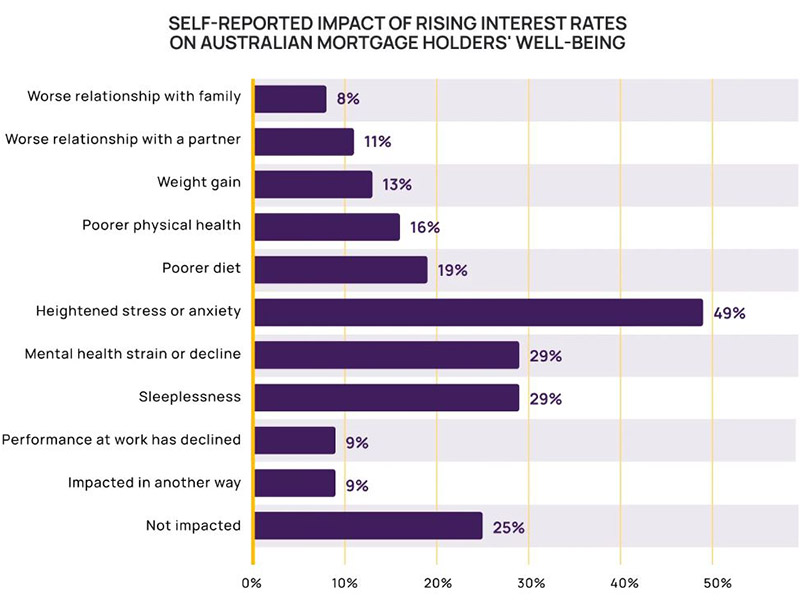

But the reality is that many Australians are feeling the mental, physical and financial strain of a dozen rate hikes since May last year and are struggling to cope with the markedly higher mortgage repayments.

Research conducted by finance platform MNY found that three quarters of Australian mortgage holders have been adversely impacted in terms of their personal lives or wellbeing.

That same 75 per cent said they would not trust any Reserve Bank of Australia (RBA) interest rates forecasts again.

With mortgage interest now averaging around 6.5 per cent, the reign of interest rate hikes means households with a $500,000 mortgage on a variable rate have seen their repayments increase by $1,500 per month in the midst of a cost-of-living crisis as their incomes are eaten away by high inflation.

Source: MNY.

Compounding the situation for those struggling is the argument that interest rates will likely rise, at least once more, before the tide turns and they begin to retreat.

Inflation is on a downward trajectory, which should bring rates down with it, but there some leading indicators that the battle against inflation may not be over.

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist, AMP Investments, said the risk in the short term is still on the upside for rates.

“In the short term, the risks are still skewed to a further increase in interest rates and or a delay in the start of rate cuts as: inflation is still too high; the labour market remains tight with upwards risks to wages flowing from higher minimum and award wage rises; productivity growth is very weak; and the rebound in home prices is partly offsetting the tightening impact of higher interest rates.

“Consistent with this, the RBA retained its guidance that some further rate hikes may be required.

“Key to watch will be the global economy, household spending, inflation and the labour market.”

Mortgage stress rampant

While the RBA has consistently stressed that Australians are well placed to manage higher interest rates after accumulating savings during Covid and paying down debt ahead of time.

But researchers are also revealing that mortgage stress is rampant.

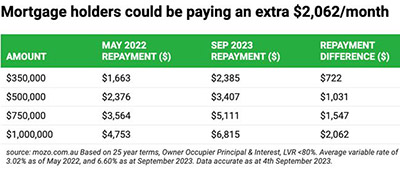

Almost half (46 per cent) of mortgage holders are now under serious financial stress, according to Mozo, as home loan variable rates starting with 5, 6 and 7 become the norm.

The average variable rate of an owner occupier home loan is now 6.60 per cent across all lenders, and 7.21 per cent across the Big Four banks.

Based on the average variable rate of 6.6 per cent, since May 2022 monthly repayments on a $500,000 home loan have increased by $1,031.

In a market where one in three borrowers think refinancing is too much of a hassle, Helen Avis, Director of Finance at Specialist Mortgage, said it was imperative those with stretched finances sought financial advice and better deals.

“The refinancing process may seem time-consuming but the savings on offer make it worthwhile and the application process these days is not as onerous as people may actually think.”

The incentive to refinance is also backed up by research from RateCity.com.au that reveals more than a quarter of Australians (27 per cent) are living payday to payday.

It found one third (33 per cent) of respondents were feeling stressed or uneasy about their budget, while 32 per cent couldn’t survive off their savings for more than a month if they were to lose their job.

Financial strain doesn’t just hit the hip pocket. The survey also found of those in a relationship, over a third (39 per cent) said cost of living concerns have caused increased friction with their partner about money.

First home buyers facing major hurdles

First home buyers are being kept out the property market, often as a result of policies that had been intended to help them.

University researchers enlisted by the Australian Housing and Urban Research Institute (AHURI) found that the path to buying a first home is increasingly reliant on parental resources.

Professor Stephen Whelan, University of Sydney, said the issues confronting first home buyers were more complex than just higher property prices.

“While high and rising house prices are often cited as the biggest challenge faced by first homebuyers, our inquiry highlights that the problem is significantly more complex,” Professor Whelan said.

“Critically, we found existing policy settings are likely to have exacerbated rather than alleviated the challenge faced by first homebuyers to finance home ownership.

“Politically seductive measures such as first homeowner grants and tax concessions have failed to arrest declining rates of home ownership over time.”

A rapid expansion of owner-occupation in the early postwar period peaked at over 70 per cent in the late 1960s but was followed by a gradually declining home-ownership rate since 2000—especially among younger adults, where the rate for the 25–34 age cohort fell from 51 per cent in 2001 to 44 per cent in 2021.

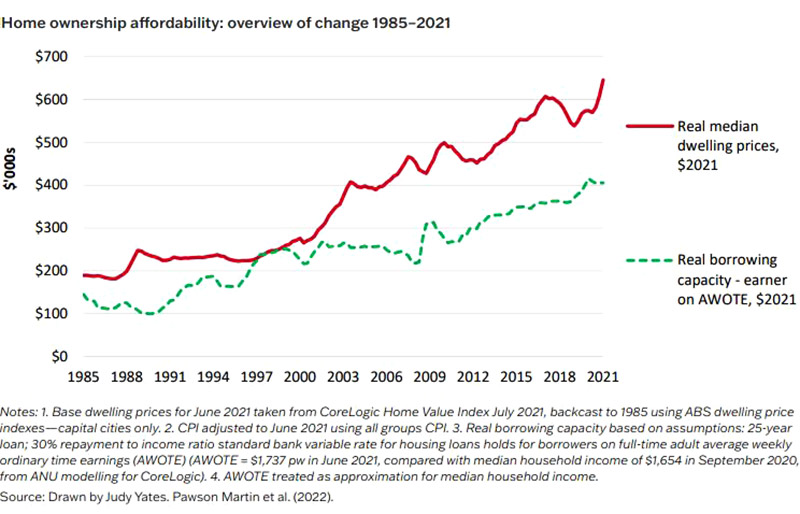

There is evidence that housing affordability has decreased over time.

AHURI’s research showed that since 2001, the national ratio of median house price to median income has almost doubled to 8.5, and the time required for the accumulation of a deposit for a typical property has increased from six years median earnings in 1994 to 14 years today.

The decline in home ownership among younger adult cohorts has occurred despite expenditures in excess of $37 billion over five decades designed to enable first home ownership.

AHURI’s findings stated that policies designed to assist first home buyers must recognise and address structural issues associated with the treatment of housing in the tax and transfer system.

“Policy settings need to encompass intermediate tenures, such as shared equity as legitimate housing outcomes that may enable households to attain homeownership,” the report said.

Article Q&A

What percentage of borrowers are in mortgage stress?

Almost half (46 per cent) of mortgage holders are now under serious financial stress, according to Mozo, as home loan variable rates starting with 5, 6 and 7 become the norm. Research conducted by finance platform MNY found that three quarters of Australian mortgage holders have been adversely impacted in terms of their personal lives or wellbeing.

Will interest rates rise or fall?

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist, AMP Investments, said the risk in the short term is still on the upside for rates, before easing in mid to late 2024.

Borrowers are refinancing in record numbers as their lower-priced fixed rate loans end, only to be switched to higher priced variable rates.

A Google analysis in 2022, conducted by a Queensland bank, found that the number of people searching the term ‘refinancing’ had increased by a staggering 5,000 percent.

Helen Avis, Director of Finance, SMATS Group

Lending indicator data released Friday (13 January) from the Australian Bureau of Statistics (ABS) shows a whopping $19.5 billion worth of mortgages were refinanced in November – the highest monthly amount in Australian history.

This figure smashed the previous record set in September 2022 by almost $1 billion.

“Recent ABS data has revealed that enormous numbers of borrowers are refinancing their home loans, indeed, the past six months have been the six biggest months in refinancing history,” Helen Avis, SMATS Group’s Director of Finance, said.

“Part of the reason so many borrowers are refinancing right now is because many lenders charge lower interest rates to new borrowers than loyal customers, as shown by Reserve Bank data.

“In October, owner-occupiers who took out new variable loans were charged, on average, 0.51 percentage points less than owner-occupiers with existing loans.

“Refinancing to a comparable lower-rate loan could potentially save tens of thousands of dollars over the life of your loan.”

Megan Keleher, Chief Customer Officer, Great Southern Bank

The source of the Google analysis, the Great Southern Bank’s Chief Customer Officer, Megan Keleher, said rising interest rates and the increased cost of living have affected household budgets and driven more customers to seek options to save on their home loans.

“They’re using the internet to find out how much they can borrow, how to refinance, and what support may be available for first home buyers.

“Using tools like a refinance calculator can really help; we’ve seen a 16 per cent increase in people using our refinance calculator over the last three months,” Ms Keleher said.

Negotiating a lower rate with their lender or switching in pursuit of a better deal is one of the best ways for mortgagees to prepare for even higher interest rates, Canstar’s Financial Services Group Executive and chief spokesperson, Stephen Mickenbecker told API Magazine.

“The Canstar Consumer Pulse Report released recently, found just a small proportion of mortgage holders (15 per cent) have switched lenders in the past year and secured a better deal, while only 8 per cent tried and failed. This means 77 per cent of borrowers could potentially be paying a lot more for their loan than what is on offer in the market today,” he said.

Stephen Mickenbecker, Group Executive, Financial Services & Chief Commentator, Canstar

Released in mid-December 2022, the Canstar report surprisingly revealed that when it came to mortgage holders coping with higher interest rates, almost one in two – 48 percent – of homeowners with a mortgage and 37 percent of investors with a loan – are unsure how much their mortgage interest rate has risen since the Reserve Bank started aggressively lifted interest rates in 2022.

“When asked how prepared they are for even higher interest rates, close to two-fifths (39 per cent) of homeowners and more than one-quarter (27 per cent) of investors are not prepared. The majority of these indicated they would need to cut their living costs further to make ends meet,” Mr Mickenbecker said.

“It’s disappointing that borrowers are not more engaged with getting a better deal, either from their own bank or by switching banks.

“Most borrowers are paying interest rates well above the relatively low rates being offered to new customers, and the monthly savings are too big to ignore.

“Borrowers can’t wait until they are unable to pay the bills to refinance into a lower rate loan as by then their desperation will be matched by lender aversion and they may find themselves out of luck with new lenders,” he said.

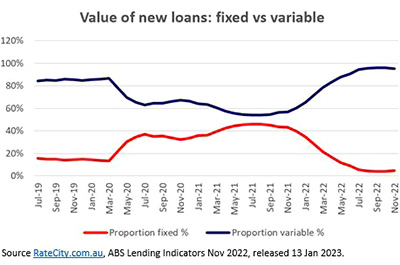

Fixed rates about to fall off cliff

As the countdown to the fixed-term cliff approaches for many property owners, few new borrowers are fixing their home loans.

The housing market, as well as borrowers, will be faced with $478 billion in fixed rates loans transferring to variable rates.

This is the so-called mortgage cliff that arises from the rollover of fixed rate mortgages taken out mid-2020 to early 2022 at interest rates around 2.5 per cent, and transitioning within the next 18 months into loans priced at 5.5 to 6 per cent. There is a large proportion of these loans falling due before the end of 2023.

“Unlike a year earlier when about half of borrowers were doing so, only 4 per cent of borrowers fixed their loans – both new loans and refinance – in October (the most recent data available).

“By contrast, 44 per cent of borrowers fixed in October 2021 and 46 per cent in August 2021, when fixing peaked,” Ms Avis said.

“While the Reserve Bank only started increasing the cash rate in May 2022, lenders knew it was coming, so they’d already started raising interest rates on their fixed- rate loans.

“In response, borrowers had begun shifting towards lower-rate variable loans.”

This is confirmed by Reserve Bank data on new owner-occupied loans.

In October 2021, the average interest rate on a new fixed loan (with a fixed period of three years or less) was 0.63 percentage points lower than a new variable loan. By February 2022, new fixed loans had become 0.09 percentage points dearer; by May they’d become 0.70 percentage points dearer.

That has since declined – by October, they were only 0.30 percentage points dearer.

Mr Mickenbecker said 39 percent of homeowners and 27 percent of borrowers polled in Canstar’s Consumer Pulse Survey in 2022 were unprepared for further rate rises.

“According to the survey, a small group of property owners (5 per cent) say they are considering selling in the next two years because they can’t afford higher loan repayments.

“While this is a small minority, the group is likely to be concentrated among more recent borrowers, with their larger loans and repayments, who have no time to have put together a buffer and have low equity.

“The impact of interest rate rises and falling property prices spreads unevenly, and recent first home buyers who overreached to get into the market will carry more than their share of the pain,” Mr Mickenbecker said.

Mortgage stress mounting

That pain will translate into falling house values and mortgage stress.

When surveyed for the Pulse Report, close to two fifths (39 per cent) of homeowners and more than a quarter (27 per cent) of investors were not prepared for higher interest rates.

The majority of these indicated they would need to to cut their living costs to make ends meet.

“If the price declines deepen to the point where many new loans in particular start falling into negative equity, the concern will heighten.

“At that stage, individuals will be feeling extreme pain and the system will be at risk,” Mr Mickenbecker said.

“With the full force of interest rate increases yet to take its toll, borrowers in particular look to be on a knife-edge, and have a limited buffer.

“A worthwhile New Year’s resolution for Australians might be to sit down and do a refresh of their household budget to work out a way to restore their financial resilience.”

Can there be high demand for housing with high interest rates?

Dr Kristle Romero Cortes, Economist and real estate markets expert, UNSW Business School of Banking and Finance associate professor

Economist and real estate markets expert, UNSW Business School of Banking and Finance associate professor Dr Kristle Romero Cortés, told API Magazine she believes housing demand can withstand these financial pressures.

“Intrinsically, mortgage rates and house prices are related via supply and demand channels. If we see that the trend is that home purchases become unaffordable due to repayments, you may see a decrease in home purchases.

“However, high-income earners need more incentive to accept lower prices when selling their homes if they can afford their repayments.

“The repayment rates would need to reach a level that selling the house now to purchase one in the future eventually becomes an attractive option.

“There has already been a move to short-term fixed loans to stabilise payment expectations. This will remain the case for borrowers; it will be interesting to see how the long-run rates on fixed loans react (3 to 5 years) because, currently, those are priced high,” Ms Cortes said.

This article, first published 11 January, was updated on 13 January with the latest ABS refinancing data.

Article Q&A

What is a mortgage cliff?

When interest rates were at historic lows during Covid, many homebuyers entered the property market on very low fixed rate loans. The terms of a large proportion of these loans end over the next 12-18 months, meaning billions of dollars in loans will switch to higher variable rate mortgages. This steep, looming rise in repayments is termed a mortgage cliff.

Is now a good time to refinance the home loan?

A Google analysis in 2022, conducted by a Queensland bank, found that the number of people searching the term ‘refinancing’ had increased by a staggering 5,000 percent. Australians refinanced $17.8 billion of mortgages in October, close to the August record volume. Property finance experts suggest now is a good time to sit down and do a refresh of the household budget to work out a way to restore financial resilience.

Experts are divided on the likelihood of an RBA interest rate cut in the next few months, but all agree borrowers are banking on it.

With inflation figures having fallen to the lowest level in almost two years, even the prospect of a cash rate rise in 2024 is up for debate.

Mortgage broker Helen Avis (pictured above left), director of Specialist Mortgage, said her clients would breathe a sigh of relief if there were no further rate hikes over the next 12 months, with many feeling the pinch of the rising cost of living.

“Many buyers are concerned about the prospect of rate increases and their ability to service their mortgage,” Avis said.

“This is particularly evident within the first home buyer market who are often shopping at their maximum borrowing capacity, investors using property as collateral to secure finance, and our overseas clients who are often faced with higher rates than Australian residents.”

High hopes that interest rates won’t rise in first half

Avis said her clients are hopeful rates will remain on hold for the next six months, with most believing they won’t see rate cuts until 2025.

“Nearly all of our clients are choosing variable loans over fixed rates. This is in significate contrast to the height of the pandemic when borrowers were opting for low-rate fixed mortgages.”

Avis said clients’ sentiment towards the property market was still positive, “but they are approaching it with a little more caution”.

She said many clients were factoring in potential rate increases, often looking at property well under their maximum borrowing capacity.

Now is a great time for borrowers to take advantage of the competitive rate market.

“Our brokers are negotiating aggressively with our clients’ existing lenders to get the best variable rates, which is often preferable compared to switching to a new loan provider,” Avis said.

Buyers need to spend within means

aussieproperty.com buyers agent Julie Kelley said rate relief would instil confidence in the property market.

“As we all know taking on too much debt can lead to unnecessary stress; I always advise clients to shop in their comfort zone,” Kelley said.

“In such a competitive market, I understand buyers can feel frustrated by not being able to secure their dream home due to budget constraints, and they may feel pressured by selling agents to quickly submit an offer above their initial budget. But it’s important not to let emotions take over.

“We always advise our buyers that are considering pushing their borrowing limits to first speak with their mortgage broker and factor in all increased costs such as stamp duty, repayments and LMI before submitting an offer on a property”.

Financial comparison site Mozo’s money expert Rachel Wastell (pictured above centre), money expert at financial comparison site Mozo, said mortgage holders would welcome a rate cut, no matter how small.

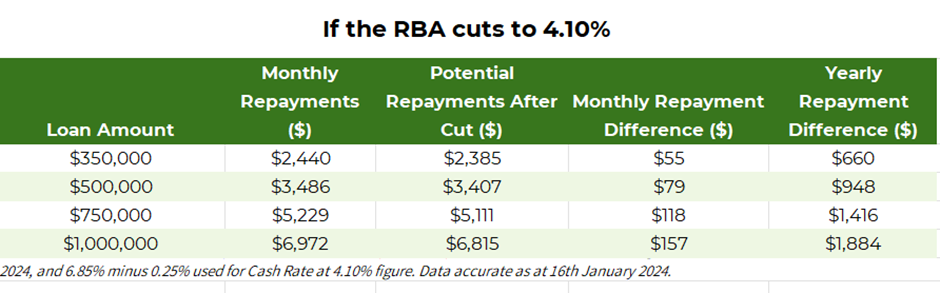

Mozo analysis shows someone with a $1 million mortgage, following a rate cut to 4.1%, will have an extra $157 a month in their pocket, equating to $1,884 a year based on the variable rate staying the same (see Mozo data below).

Source: Mozo

“I think borrowers will be cheering when a rate cut comes through,” Wastell said. “After one of the most aggressive rate hiking cycles since the early 1990s news about rates has unfortunately been quite doom and gloom.”

RBA on track to meet inflation goal?

Wastell said a rate cut will likely give borrowers some hope that the RBA is on track to meet their inflation target, and that more rate cuts could be on the horizon.

“In a cost-of-living crisis every cent counts; $100 more a month might not seem like much, but for those mortgage holders who have now resorted to credit cards or buy now pay later services to cover their everyday expenses,” Wastell said.

“That $100 could be the difference between clearing those monthly balances or being in the red.”

Despite what borrowers want, Wastell said a rate cut in the next few months was unlikely, as the unemployment rate was holding steady and inflation in services, particularly insurance, was still high.

“Later in the year, if there are no further rate hikes, and the CPI data for the June quarter shows we’re much closer to the RBA’s target of 2% to 3% we will probably see a rate cut or two, but I think it’s important homeowners don’t count their chickens before they hatch.”

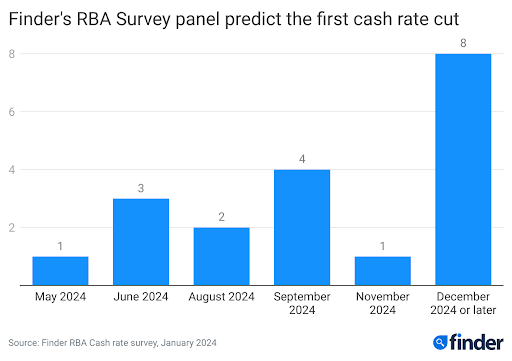

Experts predict February cash rate pause

In this month’s Finder RBA Cash Rate Survey, 19 experts and economists weighed in on future cash rate moves and almost all of the experts, 89%, said the RBA would hold the cash rate at 4.35% in February.

Head of consumer research at Finder Graham Cooke (pictured above right) said many Australians were in urgent need of reprieve following the last rate rise in November.

“Homeowners are still reeling from 13 rate hikes in the last two years,” Cooke said.

“Our data shows a staggering 40% struggled to pay their mortgage in December. Even though inflation is falling, I expect the RBA will hold the cash rate for most, if not all of 2024.”

While one in three Finder panellists predict a cash rate cut by at least August this year, almost half, or 40%, don’t expect the RBA to start cutting rates until December 2024 or later.

The majority of Finder experts, or 71%, said they expected the cost-of-living crisis to ease eventually in 2024.

“While the gauge remains in the extreme range, it’s likely that this will be where the cost-of-living pressure peaks,” Cooke said. “We expect to see some relief on the horizon, and with a little luck the pressure will reduce slowly over many months.”

Earlier this month, Bank of Queensland chief economist Peter Munckton said talk of rate increases by the RBA this year were “in the rear mirror” and said the big question for 2024 is when would interest rates start to fall.

With housing affordability at its lowest level in three decades thanks to higher cost-of-living pressures, interest rate raises and healthy property prices, Perth’s property market is proving a standout.

Helen Avis, director of specialist mortgage at brokerage SMAT Services, said Perth was experiencing a massive boom generated by younger home buyers, with housing affordability better than it was in the late 2000s and early 2010s during the height of the mining investment boom.

Avis (pictured above left) said young home buyers had shown an increased interest in the property market during the pandemic.

“But post pandemic there has been a marked decline in first home buyers in Sydney and Melbourne, which we put down to affordability, rising interest rates and the difficulties of saving for a deposit.

“The opposite can be said about Brisbane and Perth, where there is still strong demand from the first home buyer market.”

Julie Kelley, sales and marketing manager at national real estate group aussieproperty.com, (pictured above centre) said across Australia there had been an increase in the number of first home buyers attending open homes with their parents, indicating the bank of mum and dad could be the key to entering the market.

East coast investors buying lower-priced Perth property

However, Kelley said Perth property in the lower price range, particularly in the outlying suburbs, was being snapped up by east coast investors.

“Unfortunately, this is resulting in first home buyers facing more competition for homes priced under $600,000 and they are being forced to broaden their search to the outskirt suburbs or consider buying smaller apartments and cottage homes,” Kelley said.

“The biggest increases in enquiries are from investors and buyers looking to upgrade their homes.

“There has been an enormous increase of interstate interest in Perth real estate particularly from Sydney and Melbourne.

“We have also seen a record night numbers of interstate migration and given Perth’s vacancy rate of 0.9% it’s difficult to secure rental properties, so many cashed up eastern states’ migrants are looking to purchase. “

Avis said many interstate buyers were guided by buyers’ advocates with limited local area knowledge or by big data, which could lead to poor long-term investment decisions.

“Off-the-plan developments hasn’t been popular for the past 12 months mainly due to the risk factors associated with the current state of the building and construction industry,” Avis said.

“Inner city suburbs and the western suburbs are still the most desirable locations for owner occupiers and investors, the north west coastal suburbs are also very popular.

“They are well established suburbs, close to the river and ocean, have excellent amenities, recreational facilities and public transport to the CBD and universities.”

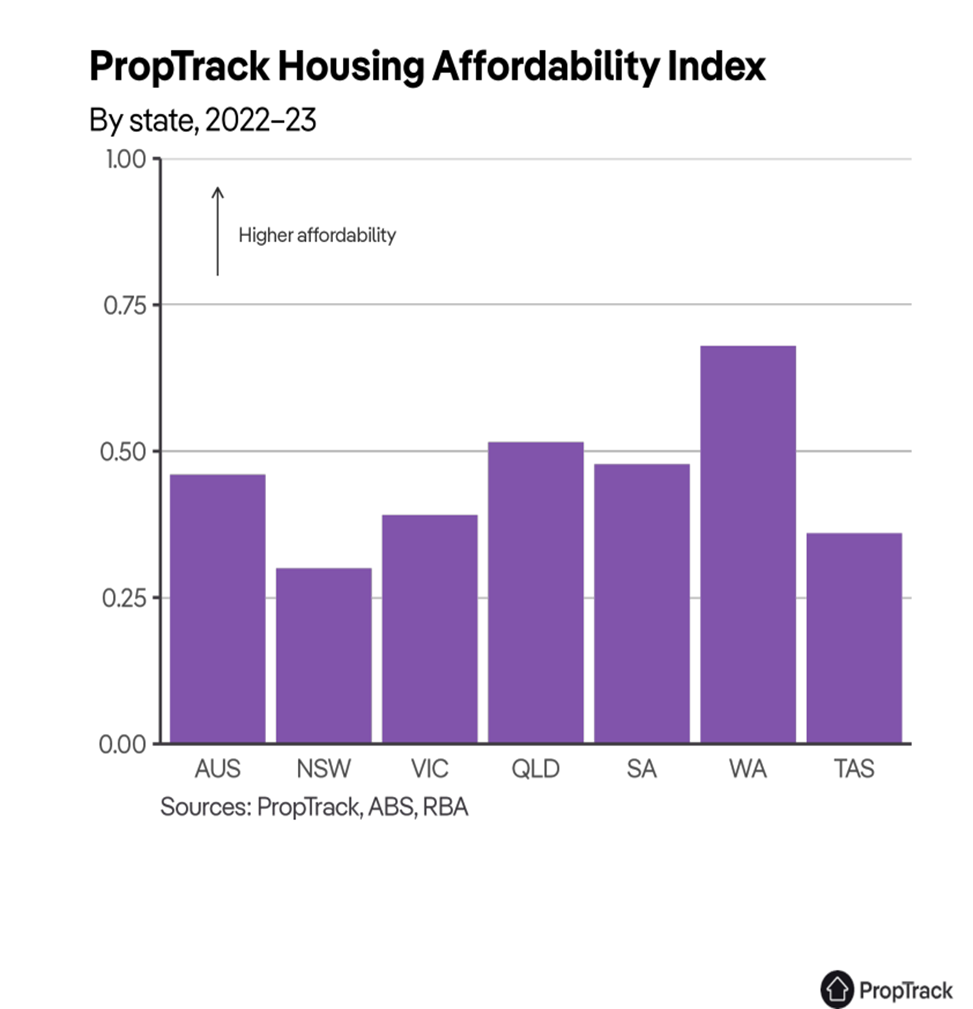

A recent PropTrack Housing Affordability Index 2023 report highlights just how dire affordability is now particularly in NSW, Tasmania, and Victoria, with Perth the most affordable state in Australia.

“That is a marked change from a decade ago, when Western Australia was the least affordable state from 2007-2010 amid the height of the mining investment boom,” the report states.

“[This is] the only time any state has displaced NSW as the least-affordable state.”

Peter Gavalas, a buyer’s agent from Resolve Property Solutions, (pictured above right) cautioned that fierce buyer competition amid the booming Perth property market could see some buyers settle for low-quality properties that they might one day regret owning.

“The bottom line is that, right now, the Perth property market doesn’t have enough supply to cater to all the demand,” Gavalas said.

“So buyers are reacting the same way they do in any boom – they’re compromising on quality, by settling for less desirable homes, such as ones with structural problems, or less desirable locations, such as on noisy main roads, because they fear they’ll never enter the market any other way.”

Gavalas said even though buyers were experiencing FOMO, it was likely they would suffer a case of buyer’s remorse in the years ahead if they compromised on quality.

“A better option would be to buy a higher-quality property with stronger resale value in a cheaper neighbouring suburb,” Gavalas said.

Specialist Mortgage finance director Helen Avis has been recognised in this year’s MPA Top 100 list, as one of the Top Mortgage brokers writing the highest value of loans in FY21; further adding to a long history of achievements and awards in the Australian finance industry.

Ms Avis settled a staggering $153 million in loans for FY21, a 67% increase on the previous year with no signs of slowing down. Signing 249 loans to rank in the Top 25, considerable momentum started to gather steam around September 2019. 2022 is looking to be even more successful, off the back of a personal record set in July 2021 settling more than $25 million across 29 deals.

“Over the past 12 months the market has become hugely competitive and experienced a meteoric rise in housing values. Unprecedented low-interest rates have not only attracted homebuyers but also resulted in property investors returning to the market along with high levels of refinancing.”

“A lot more buyers were acting and buying property than they were previously, whether as owner-occupiers, future owner-occupiers or as investors,”

“The sheer volume of people, the speed of the market and price points have been phenomenal. Economists are predicting a slowdown in the property market however I’m not seeing any signs of it yet.” Ms Avis added.

More than 600,000 Australians have returned home from international cities since the onset of COVID-19. The appeal of Australia being a safe haven has seen a demand for family homes gain momentum particularly in Queensland, Melbourne and Sydney.

Having experienced the trials and tribulations as an expat herself, Ms Avis has established a trusted position within the expatriate community and understands securing attractive Australian finance options for expats is not only difficult but often a complicated process whilst residing overseas.

‘The last 12 months was not without challenges, with banks taking extended times to process applications throughout the pandemic,’

“For expats we have limited lenders with attractive terms and often longer processing times. The market is fiercely competitive, in some circumstances, buyers have had to make a choice between securing the lowest rate or the quickest loan processing time.”

Setting herself apart from other brokers as a specialist in expatriate finance with her extensive experience and knowledge of expat financial package terms and conditions, Ms Avis’ ability to successfully communicate to banks to get finance approved quickly makes her a leader in the field.

“I am very optimistic for the next few years,”

“We are likely to see more expats returning, more interstate moving, migrants finally moving to Australia, and international students coming back will help the rental market in the cities of Melbourne and Sydney.

“One positive taken away is the importance of being compassionate to clients, especially those who have faced job uncertainty and financial distress or have experienced delays in getting loan documents signed and notarised through lockdown restrictions.”

Having a career spanning more than three decades, Ms Avis has built a reputation on her tenacity to respond promptly and professionally and working tirelessly to secure the best financial packages for her clients.

The lessons learnt through the pandemic are ones Ms Avis says will carry the Specialist Mortgage team in good stead for the future, understanding there is no substitute for hard work and looking forward to continued growth in 2022.

Helen Avis, winner of the prestigious MFAA Residential Finance Broker Award, said interest rate concerns were beginning to weigh on the minds of clients but business was still strong as buyers remained highly active in the real estate market.

he Mortgage and Finance Association of Australia (MFAA) Awards have named Helen Avis of Specialist Mortgage (part of the SMATS Group of Companies) winner of the national Residential Finance Broker Award.

The winners of the MFAA National Excellence Awards 2022 were recently announced at a glamorous event at The Star in Sydney.

The MFAA National Excellence Awards acknowledge brokers, lenders, aggregators and industry professionals who have demonstrated exceptional customer service, professionalism, ethics, growth and innovation.

Ms Avis said the award was the culmination of more than two decades building a business with her husband, Steve Douglas, Executive Chairman of SMATS Group.

With offices in Australia, Singapore, Hong Kong and the Middle East, Ms Avis and the Specialist Mortgage team specialise in securing mortgages and consolidating loans for Australian expatriates and foreign investors who are often faced with limited affordable options from Australian and overseas lending providers.

“I am honoured to be recognised by my industry peers and named as the winner of this award. I love what I do. Helping people secure their home or investment property gives me so much satisfaction.”

Ms Avis, who won the Western Australian state award, settled a staggering $187 million in loans for 2021, a 67 per cent increase on the previous year with no signs of slowing down.

2022 is looking to be even more successful, off the back of a personal record set in July 2021 settling more than $25 million across 29 deals.

Going ballistic

Speaking to API Magazine, Ms Avis said this year had been challenging because of the interest rate hike cycle being undertaken by the Reserve Bank of Australia, but the market had heated up again.

“We noticed after the 0.5 per cent rate rise in June, that enquiries appeared to slow down, however I believe, buyers were just being cautious and wanted to see the impact on property prices.

“Since then, our enquiry rate has gone ballistic again, with home buyers and investors locally and overseas wanting to buy.

“Many buyers believe property prices will decrease but our clients report that homes located in highly desirable suburbs are still attracting a lot of interest and competition at auction.

“It will be interesting to see how the rapid interest rises impact buyer activity, days on market and property prices.

“I am also expecting to see more clients looking to purchase as a result of interstate and overseas migration.”

Concerns about interest rates were on clients’ minds and they have voted with their feet when choosing their loan type.

“Up until October last year the majority of our clients secured fixed rate loans, but when fixed rates started going up clients were opting to split loans, now almost all of my clients are selecting variable rate loans.”

Helen Avis, Director, Specialist Mortgage, has added another accolade to her impressive list of achievements, this time securing the Western Australian customer service award for an individual at The Adviser Better Business Awards.

On a night when the who’s who of Western Australia’s broking industry were rewarded for their achievements at The Adviser Better Business Awards, Finance Director of Specialist Mortgage, Helen Avis, took home the coveted Best Customer Service (Individual) Award.

In presenting the prestigious award, judges praised Ms Avis for “her outstanding submission that demonstrated her innovation, communication, and notable growth rates.”

The Specialist Mortgage team was also named as a finalist in the Best Customer Service (Office) Finalist category, while Ms Avis was a finalist in a second category, Best Residential Broker.

Speaking after her win, Ms Avis said 20 years of experience and an innate understanding of her clients’ needs, financial situations and aspirations was at the core of her success.

Ms Avis, who recently won the national MFAA Residential Finance Broker Award, said she went above and beyond in ensuring her advice delivered the best interest rates and took into account the many variables that go into securing the best financial package for her clients.

She added that 2023 shaped as another busy year, as she helped clients navigate the financial landscape as they confronted a forced shift from low interest fixed rate loans to higher variable rates, or the so-called mortgage cliff.

“A lot of clients are in this situation and we send them reminders that the new loan arrangement is coming and diligently work with them to plan accordingly.”

“It’s another hectic year ahead and we really look forward to helping clients, and that extends to their whole family, to get the best possible deal on their mortgage by benefiting from our experience, knowledge, contacts and commitment,” Ms Avis said.

Established in 1991, Specialist Mortgage provides all types of lending options to Australian property investors.

On the night, 97 finalists who were in the running for 19 awards, including brokers and brokerages, business development managers (BDM), and loan administrators as well as thought leaders and mentors.

The awards, run in partnership by The Advisor and NAB, are in their tenth year.

Winner announcements were featured in The Adviser.

Specialist Mortgage, part of the SMATS Group, won the prestigious Finance Broker Business Award WA category in the Mortgage and Finance Association of Australian (MFAA) Excellence Awards.

Specialist Mortgage has been named winner of the Finance Broker Business Award WA in the Mortgage and Finance Association of Australian (MFAA) Excellence Awards 2023.

The award was presented at a glittering event held at Crown Perth on Thursday night (15 June), where Helen Avis, Director of Finance at Specialist Mortgage, was also recognised as a finalist in the Customer Service Award – Individual category.

As the Western Australian state winner, Specialist Mortgage becomes a finalist in the National Awards to be held on 27 July in Melbourne.

The MFAA Excellence awards are considered a pinnacle of prestige and recognition within the mortgage and finance industry. The awards are audited by Hall Chadwick accounting firm and are judged based on excellence and professionalism across all areas of business.

MFAA CEO Anja Pannek commented that the competition was strong this year as she congratulated winners and finalists at the awards ceremony.

“The phenomenal number of nominations for the MFAA Awards this year made a difficult task for our judges, but showed just how vibrant our industry is,” Ms Pannek said.

There are 24 award categories that cover brokers, businesses, lenders and support staff. The qualifying period is 1 January 2022 to 31 December 2022.

All entrants have submitted examples and evidence in earning their place on the winners’ rostrum.

Ms Avis said interest rates had an effect on the market but property transaction activity was still strong.

“The market is still super strong among buyers all over Australia, including investors, expats buying homes for use in the future, and residents buying first or second homes.

“Of course the higher interest rates mean that lending has reduced but also in some cases clients have had an increase in pay, or bonus that can be used to counterbalance that cost increase,” Ms Avis said.

The event’s sponsors included MPA Magazine, as well as ANZ, BOQ, Commonwealth Bank (CBA), Helia, La Trobe Financial, Macquarie Bank, ME Bank, Mortgage Choice, NAB, Prospa, QBE and Teachers Mutual Bank.

In the dynamic realm of finance, attending industry conferences is not just an option; it’s a strategic move towards growth, innovation, and personal and professional development. This sentiment was vividly echoed at the recent SFG National Conference and Awards in the tropical paradise of Port Douglas.

So why have industry conferences? Do they matter?

As industry leaders, our commitment to excellence extends beyond our daily operations. It involves staying abreast of industry trends, fostering innovation, and building a team that thrives on knowledge and inspiration. Industry conferences like the SFG National event offer a rich tapestry of experiences, from captivating speakers to engaging panel sessions and unique team-building activities.

Last weekend I had the absolute pleasure of inviting my team to come along to the SFG National Conference and awards presentation in Port Douglas and it really did not disappoint. It kicked off with a bang on Day 1, immersing attendees in mind-bending experiences with Anthony Laye’s mind reading and Bastien Treptel’s IT hacking skills. The inspirational keynote by explorer Justin Jones set the tone for a conference focused on pushing boundaries. The day concluded with a Lender Panel Session that deepened our industry insights, followed by a laid-back Tropical beach BBQ—a stellar start to an industry event!

Day 2 commenced with sunrise reflections on Four Mile Beach, setting the stage for profound insights. Australian racing legend Craig Lowndes shared his success journey, complemented by sessions with young trailblazers and industry leaders. Award-winning Engagement & Thought Leader, Dan Gregory, enriched our perspectives on connected purpose and creativity. The day culminated with anticipation for the SFG National Awards.

An absolute triumph! -celebrating Success and Camaraderie

Under the starlit skies of Port Douglas, the SFG National Awards unfolded on Day 3. The moment of pride arrived as I’m very humbled to report on receiving the coveted WA Broker of the Year award. A testament to a year marked by dedication, expertise, and outstanding achievements. The awards ceremony was a fitting conclusion to an eventful year and a prelude to the exciting prospects of 2024.

To cap off the celebration, attendees relished the SFG High Achievers Event, a blend of sophistication and relaxation. A visit to the Devil Thumbs Distillery and the Trinity Beach Palace set the stage for a delightful long-table lunch, marked by laughter, camaraderie, and shared successes. It was a day of acknowledgment, not just for individual achievements but for the collective triumphs of the finance & mortgage community on what has been a tumultuous year.

In closing, a heartfelt thank you to the entire SFG Team for orchestrating a weekend of learning, recognition, and celebration. As we raise a toast to 2024, we carry with us the lessons learned, the bonds forged, and the inspiration gained from the SFG National Conference and Awards—a pivotal milestone in our journey toward continued success. Cheers to a year of growth, collaboration, and prosperity!

International buyers are still eyeing off Australia as a great place to invest in property with New Zealanders the most active, while Chinese investors are showing a renewed interest, according to a new report.

“Perth is a beautiful city. Our lifestyle and weather are the most desirable in the world,” Avis said.

“Our economy and job market are strong; wages are generous, and our school system is attractive for families, and we are a politically stable and safe place.

“Who doesn’t want to lap up the sunshine and endless coastline that Perth has on offer?”

According to Avis, Perth is one of the most affordable capital cities in Australia with a median house price is $570,000, according to property site REIWA.

“With a budget of $1 million, buyers are able to secure a lovely four-bedroom, two-bathroom home in a desirable suburb close to the city. When you compare that to the east coast, a $1 million budget doesn’t stretch very far at all, for example the median price in Sydney is $1,098,821 (according to CoreLogic).

“The price of housing and cost of living are certainly attractive to migrants.”

According to Avis, population growth and dire housing supply shortages are the key factors driving the Perth property market now.

“The distinctive disparity between supply and demand is rapidly forcing housing values upward,” Avis said.

“WA is experiencing the fastest population growth rate of any Australian state and territory. Our population grew by 2.8% to 2.855 million in the year to March 2023.

“The March quarter saw one of the biggest recorded population increases at 0.9% (according to the ABS). We are certainly seeing an influx of overseas and interstate migration.”

Avis said because Perth’s rental vacancy rate was below 1%, it was challenging for migrants to secure rental properties so ‘this has resulted in higher interest in purchasing property from this market segment’.

She said apart from strong interest in Perth properties from investors from the east coast of Australia, Australian expats in South East Asia, Dubai, London and US also showed a keen interest in the WA capital’s property sector.

“We are experiencing increased interest from USA, UK and NZ migrants, as well as Sydney, Brisbane and Melbourne looking to relocate. “