Undeterred by property prices in Melbourne and Sydney coming off the boil or the threat of higher interest rates, expatriate Australians are continuing to snap up prestige properties.

Undeterred by property prices in Melbourne and Sydney coming off the boil or the threat of higher interest rates, expatriate Australians are continuing to snap up properties priced considerably higher than median city values.

Helen Avis, the SMATS Group Director of Finance, said the expatriates that had recently returned to Australia were moving from rentals into their own properties and could afford prestige real estate in highly sought-after areas.

“The $2 million to $4 million bracket has been very active as expats plan their eventual return and want to buy the future home, or move from their temporary rentals having recently returned,” Ms Avis said.

The recently-name finalist in the national Better Business Awards, in Best Residential Broker category, said she had also seen a lot of buyers targeting regional areas, holiday locations and the holiday home market.

“There’s very little investor or expatriate interest in CBD city apartments – that market has dried up – but there is still a lot of demand for luxury apartments as well as houses in the higher-priced suburbs.”

The first quarter of the year has seen Australian dwelling values rise by 2.4 per cent, less than half the pace of the same period last year.

But expatriates seeking a home rather than an investment can afford to pay the premiums that two years of rapid price growth has delivered and are not phased at the prospect of higher interest rates.

Interesting times

The big four bank economists are forecasting official cash rate hikes could begin between June and September.

Not waiting for the Reserve Bank of Australia, Australia’s third and fourth largest banks, NAB and ANZ, on Friday (1 April) hiked fixed rates by up to 0.40 percentage points.

“We have seen all banks raise fixed rates so many times in the last six months and I expect the RBA will raise rates from June,” Ms Avis said.

Helen Avis, finalist in the Better Business Awards

“I don’t think they want to raise them and then continue to raise them regularly, so it should be a slow progression, but the market is expecting interest rates to rise.

“All borrowers are assessed at 3 per cent over the benchmark rate, so it shouldn’t put stress on people’s ability to maintain their loans.

“With the borders just opening back up, we should have a two-year backlog of intended migrants, expats and international students start to push up the rental market as well as CBD sales.

“The intended migrants will likely rent to start off with, but most will likely want to buy, so demand will again be strengthened.”

Ms Avis said SMATS Group’s aussieproperty.com had clients looking at all states’ markets but Queensland was generating the most interest.

Sydney, Melbourne, Perth and the West Australian southwest were also on the radar of returning expatriates, she said.

The Better Business Awards seek to champion the leading players of the broking industry in each state and territory of Australia.

Reaching the finalists stage is regarded as an incredible achievement across the Australian broking industry, showcasing the depth of dedication and commitment each individual and team brings to advancing the industry.

Ms Avis said she was humbled to be recognised and proud to be named as a finalist. Winners are announced at a ceremony on 19 May.

A slight improvement in vacancy rates has done little to quell the rental crisis, while a disturbing proportion of home owners are also doing it tough and missing mortgage repayments.

Any joy renters might have had that there had been a fractional improvement in vacancy rates around the country have been extinguished by rents still rising.

For home owners struggling to pay the mortgage, the picture is no brighter.

New research has shown that a worrying one in eight borrowers has missed one or more payment deadlines in the past six months.

An additional 32 per cent of borrowers who did pay on time told the Finder survey that they were worried a missed payment was looming as a scary possibility.

Renters have arguably been the hardest hit cohort of Australians as the cost of living and housing crises have become increasingly problematic.

In a glimmer of good news was PropTrack’s Thursday data showing the share of available rentals further increased in May, with the national rental vacancy rate up 0.08 percentage points (ppt) to 1.30 per cent.

(Source: Ray White Group/ABS)

This is the highest rental vacancy rate since July 2023, and the first instance of three successive monthly improvements since late-2020.

With overseas migration and student visa applications having peaked, the number of prospective tenants per rental property slightly easing, and more renters entering shared housing options to reduce costs, these factors combined could help to relieve some pressure on the rental market.

According to Rent.com.au statistics released Wednesday (5 June) there was a 7.1 per cent increase in the number of rental properties available nationally in May 2024.

All states and territories recorded increases in rental listing volumes, however, the vacancy rate in Darwin dropped 0.3 per cent to 1.1 per cent in May.

The very modest improvement in vacancy rates the remain chronically tight there was still a 1.7 per cent rise in rents nationally, from $600 to $610 per week. The highest increase in median house rent was recorded in Brisbane (+3.2 per cent; +$20 to $650) while the largest fall was in Canberra (-4.2 per cent; -$30 to $690).

The critical undersupply of current and new rental properties, along continued strong demand and rental price growth, means that it will still be tough going for renters and the rental market will remain extremely challenging for the rest of 2024.

Paul Ryan, Senior Economist, PropTrack, said that while any easing in conditions will be welcomed by renters, available properties remain very scarce with the vacancy rate at around half the levels seen before the pandemic.

“This means competition for rentals will remain strong and rents will continue to increase.

“The easing in conditions over the past three months has been most evident in Perth, Sydney and the ACT, with Perth seeing a substantial improvement after very tough conditions recently.

“While availability remains low across all markets, Adelaide and Brisbane remain the toughest for renters, with rental vacancy rates of 1.03 per cent and 1.11 per cent, respectively.

“We expect renters will face continued difficulty securing rentals and strong rent price growth over the rest of 2024 in these markets,” Mr Ryan said.

Borrowers trying to make ends meet

A worrying number of homeowners are struggling to keep up with their mortgage repayments, according to new research by Finder, Australia’s most visited comparison site.

A Finder survey of 1,071 respondents – 342 of whom have a mortgage – revealed 12 per cent have missed one or more repayments over the past six months.

That’s an estimated 396,000 borrowers who have fallen behind on their mortgage.

The research found 4 per cent of mortgage holders – 132,000 households – say they have missed one repayment.

A further 8 per cent of mortgage holders – 264,000 households – have missed more than one repayment.

The data revealed 3 per cent have had to ask for a repayment holiday or applied for hardship from their lender.

Richard Whitten, home loans expert at Finder, said mortgage defaults were a growing concern.

“Thousands of mortgage holders have weathered rate rises but are now experiencing extreme financial strain as savings and emergency funds run dry.

“Any further hikes would push many to breaking point.”

Shockingly, 1 in 3 borrowers (32 per cent) are worried they will miss a repayment due to mortgage stress. That’s over 1 million Australians at risk of delinquency.

Of those who missed a repayment, a third (33 per cent) said they ran out of money because of other bills, while 31 per cent said interest rates increased and they could no longer afford it.

Whitten said many Aussies are forking out a disproportionate amount of their income paying off their home loan.

“Interest rates rose so rapidly that mortgagors have reached breaking point with some unable to stay financially afloat.”

Variable rate loans remain the near-unanimous choice of borrowers, according to Helen Avis, Director, Specialist Mortgage.

Back in March 2020, at the start of the pandemic, 13.38 per cent of new borrowers were choosing fixed-rate loans and 86.62 per cent were choosing variable. But in March 2024, a staggering low of only 1.40 per cent of new loans were fixed, compared to 98.60 per cent variable, according to the Australian Bureau of Statistics.

According to data released by Ray White on Wednesday (5 June), Melbourne contains all ten of the top 10 list of suburbs with the most house rentals listed under that benchmark price.

The list is slightly more diverse for renters looking for units. Of the top 10 most affordable suburbs, half come from Melbourne, three come from Adelaide, while Hobart and Sydney offer one.

Atom Go Tian, Senior Data Analyst, Ray White Group, said the share of median asking rent versus weekly earnings was 40.5 per cent for houses and 38.4 per cent for units.

According to ABS, average weekly earnings as of November 2023 was $1,431 per week, a 35 per cent increase from 10 years ago. During the same period, rent has outpaced our growth in earnings with the median asking rent for houses growing by 56 per cent to $580 and the median asking rent for units growing by 52 per cent to $550.

Mr Tian said the balance between real income and rent costs has shifted dramatically, with the past two years having crunched renters.

“For the first eight years of the last decade, the share of rent versus earnings stayed relatively flat between 33 and 35 per cent.

“Weekly earnings growth even outpaced rent growth, with the share of rent reaching its lowest point in 2020 for houses at 32 per cent of weekly earnings and in 2021 for units at 31.4 per cent of weekly earnings.

“Since then, however, rent has skyrocketed.”

Meanwhile, on the rental supply front, the Property Council of Australia on Wednesday welcomed the introduction of the Treasury Laws Amendment (Responsible Buy Now Pay Later and Other Measures) Bill 2024 as recognising the role of build-to-rent (BTR) housing in Australia but warned it does not create a level pathway to support 150,000 new BTR homes by 2034.

Article Q&A

What is the national vacancy rate in Australia?

PropTrack’s June 2024 data shows the share of available rentals further increased in May, with the national rental vacancy rate up 0.08 percentage points (ppt) to 1.30 per cent.

Are borrowers defaulting on mortages?

New research has shown that a worrying one in eight Australian borrowers has missed one or more payment deadlines in the past six months. An additional 32 per cent of borrowers who did pay on time told a Finder survey that they were worried a missed payment was looming as a scary possibility.

Are rents still rising in Australia?

In May 2024, there was a 1.7 per cent rise in rents nationally, from $600 to $610 per week. The highest increase in median house rent was recorded in Brisbane (+3.2 per cent; +$20 to $650) while the largest fall was in Canberra (-4.2 per cent; -$30 to $690).

Which Australian city is the cheapest to rent in?

When it comes to suburbs with rental listings under $500 per week, nowhere comes close to Melbourne. According to data released by Ray White on 5 June 2024, Melbourne contains all ten of the top 10 list of suburbs with the most house rentals listed under that benchmark price.

Commentators were unanimous in their expectations the Board would sit tight in the face of stubbornly high inflation but is an interest rate shock in the pipeline?

The RBA continues to perform its balancing act of trying to contain inflation without causing an economic hard landing.

Given all 38 commentators in a Finder survey tipped a rate hold, the decision to retain the official cash rate at 4.35 per cent at its Tuesday (18 June) meeting comes as no surprise.

The RBA did, however, say it won’t tolerate high inflation indefinitely.

The recent falls in the inflation rate reversed last month, when it inched up and spooked borrowers hoping its continued decline would mean a rate cut was imminent.

But short of a major international economic shock that rattled the local economy, a rate cut now seems a distant prospect.

There have been 13 interest rate increases since May 2013 but the latest decision marks the fourth successive hold.

The holding pattern may run for some time yet, although the RBA made it clear that economic uncertainty could see it spring a surprise if that was necessary to contain inflation. Borrowers will have to wait until 6 August for the next RBA meeting.

Australians spending money they don’t have

In making its decision, the RBA indicated it is keen to see the positive of lower unemployment rates continue and mass job losses avoided, but with spending levels contained to ensure inflation fell to within its preferred band of 2 to 3 per cent.

There are worrying concerns that spending is continuing in the face of cost of living pressures and heightened levels of loan delinquency.

Worldpay’s Global Payments Report 2024 revealed buy now pay later (BNPL) use is at an all-time high in Australia – accounting for 15 per cent of eCommerce transaction value in 2023.

Almost half of experts who weighed in (44 per cent) say the current level of BNPL use is alarming.

Finder’s Consumer Sentiment Tracker shows two in five (42 per cent) Australians have used a BNPL service in the past six months.

Those who have used BNPL are carrying an average of $1,073 in debt, up from $916 in 2022.

Spending on property also appeared unlikely to be curtailed in the short term.

Helen Avis, Director of Finance, Specialist Mortgage, said rising property prices were unlikely to be stifled by the RBA.

“With the high migration there is not enough supply, while we have also seen an exodus from Sydney to regional NSW and Queensland that has applied price pressure to those markets.

“So despite the fact that rates are high we are still seeing people buying.

“I had a period earlier this year where my clients were ‘wait and see’, but recently they have had the confidence to buy.

“Some people have cut back on spending and adjusted their finances to manage the increased cost of their mortgages and also the cost of living, but overall clients seem to be coping with the current market conditions.”

RBA keeps it short and sweet

In the RBA’s shortest Monetary Policy Decision in this reporter’s memory, inflation and economic uncertainty were its key themes.

“Inflation is easing but has been doing so more slowly than previously expected and it remains high,” the Board’s statement noted.

“The Board expects that it will be some time yet before inflation is sustainably in the target range (and) while recent data has been mixed, they have reinforced the need to remain vigilant to upside risks to inflation.

“The path of interest rates that will best ensure inflation returns to target in a reasonable timeframe remains uncertain and the Board is not ruling anything in or out.”

On the economic front, the RBA suggested it could be a bumpy road ahead, noting that, “the economic outlook remains uncertain and … the process of returning inflation to target is unlikely to be smooth.”

The possibility of another rate increase is on the cards and that will push many mortgage borrowers over the edge, and take many other Australians with them.

– Peter Boehm, Pathfinder Consulting

Conceding that economic momentum was weak, savings rates and high spending were weighing more heavily than slow GDP growth, a rise in the unemployment rate to 4 per cent and slower-than-expected wages growth.

“There are uncertainties regarding the lags in the effect of monetary policy and how firms’ pricing decisions and wages will respond to the slower growth in the economy at a time of excess demand, and while conditions in the labour market remain tight,” the RBA noted.

There also remains a high level of uncertainty about the overseas outlook.

“Output growth in most advanced economies appears to have troughed.

“There has been improvement in the outlook for the Chinese and US economies, and many commodity prices have picked up.

“Some central banks have eased policy, although they remain alert to the risk of persistent inflation.

“Nevertheless, geopolitical uncertainties, including those related to the conflicts in the Middle East and Ukraine, remain elevated, which may have implications for supply chains.”

Where the experts expect interest rates to head

The consensus among economists is that rate hikes are finished and the next move from the RBA will be a cut, but the timing is highly uncertain.

Financial markets, based on the ASX cash rate futures, have brought forward the timing of a rate cut from around mid-year 2025 to a fully priced in cut by March of next year. Meanwhile three of the big four banks’ economic units are forecasting a 25 basis point cut in November 2024.

Housing markets seem to be somewhat insulated from higher interest rates, with CoreLogic’s Home Value Index continuing to rise through June, and the combined capitals daily index already 0.4 per cent higher over the first 18 days of the month.

“The RBA made a point of calling out an increase in household wealth via higher housing prices which, together with a rise in disposable incomes, could support household spending,” Tim Lawless, Research Director at CoreLogic Asia Pacific, said.

“Similarly, the volume of home sales is tracking higher than a year ago and above the five-year average, demonstrating consistently strong demand from purchasers despite an array of headwinds including high interest rates, cost of living pressures, low sentiment and stretched affordability.”

The RBA had reason to be patient, according to Matthew Greenwood-Nimmo, Associate Professor of Economics, University of Melbourne.

Matt Greenwood-Nimmo, Associate Professor of Economics, University of Melbourne

“Although inflation is still stubbornly high, the RBA is likely to hold the cash rate constant in the near term.

“There are signs of weakness in the economy, and the full impact of past rate hikes is yet to be fully felt,” he said.

Jakob Madsen, Economics Professor at University of Western Australia, pointed to international conditions propping rates up for now.

“The US Federal Reserve fund rate is still more than 1 per cent point above the RBA cash rate and the increasing worldwide government debt-to-GDP ratio is keeping upward pressure on interest rates.”

There is no justification to reduce rates based on current economic data, according to Peter Boehm, Managing Director, Pathfinder Consulting.

“The pendulum is swinging towards an increase because of sticky inflation and a government fiscal policy that is likely to put upward pressures on inflation.

“Plus, I doubt there is a single Australian right now who is not suffering from sustained and ongoing price increases in such areas as utility/energy, health, food and just general living costs.

“By way of example, many charities cannot keep up with demand due to an increasing number of families struggling to put food on the table or cover essential living expenses.

“The possibility of another rate increase is on the cards and that will push many mortgage borrowers over the edge, and take many other Australians with them.”

Article Q&A

What is the official cash rate in Australia?

There have been 13 interest rate increases since May 2013 but the June 2024 RBA decision marks the fourth successive hold at 4.35 per cent.

The Mortgage and Finance Association of Australia named Ms Avis Residential Finance Broker WA 2024, marking her second time atop this podium.

The mortgage and finance broking industry in Western Australia honoured this year’s achievers at the 2024 MFAA State Excellence Awards, with Helen Avis, Director of Finance, Specialist Mortgage, taking out one the most coveted awards for the second time.

The Mortgage and Finance Association of Australia named Ms Avis Residential Finance Broker WA 2024.

Ms Avis said the MFAA Excellence Awards are renowned for celebrating the highest standards of professionalism, integrity, and innovation in this finance field.

“This recognition is a significant milestone in my career, and I am deeply grateful for the acknowledgment of my hard work and dedication within the mortgage and finance industry,” Ms Avis said.

“Winning this award is not just a personal achievement but also a testament to the incredible team and clients I have had the privilege to work with.”

Ms Avis added that the award highlighted the significant contributions of women in the mortgage industry.

“It is a powerful reminder that with determination, passion, and the right support, we can achieve great heights.

“I hope this recognition inspires other women in our industry to pursue their goals with confidence and resilience.”

All Western Australia MFAA State Excellence Awards winners are finalists in their respective categories at the MFAA National Excellence Awards which will be held in Melbourne on Thursday 25 July following the MFAA National Conference.

Advice for borrowers struggling with deposit

While it’s often said a 20 per cent deposit is needed to qualify for a home loan, a significant number of borrowers are securing mortgages with smaller deposits, according to the latest data from APRA, the banking regulator.

Ms Avis said it was still possible to buy a property with a small deposit and could offer advice on structuring a loan application correctly.

In the March 2024 quarter, 31.0 per cent of new home loans (by value) had deposits of less than 20 per cent, while 6.2 per cent of new loans had deposits of less than 10 per cent.

“While more than three in 10 borrowers are taking out loans with deposits under 20 per cent, these figures are relatively low by historical standards.

“Back in December 2020, for example, 41.7 per cent of new loans had deposits of less than 20 per cent, while 11.3 per cent had deposits of less than 10 per cent.

“This illustrates how banks have tightened their lending standards, to ensure borrowers don’t take on an excessive amount of debt, yet it’s still possible to buy a property with a small deposit,” Ms Avis said.

Generally, these buyers will need to pay lender’s mortgage insurance (LMI) when purchasing a property with a deposit of less than 15-20 per cent.

Home buyers will be contemplating more expensive property purchases with their increased borrowing power, while mortgagees will be hoping to bolster their loan repayments, with the Stage 3 tax cuts coming into effect.

As the new financial year begins, millions of Australians will be feeling a sense of mild relief that they have received a cut to their tax rate.

But as well as having an average of $1,888 extra on their annual income statement, for many Australians it will be welcomed for another reason.

For home buyers, the Federal Government’s Stage 3 tax cuts are set to receive a boost in borrowing power. Those already on the property ladder could slice years off their mortgage.

The tax cuts reduce the 32.5 per cent tax bracket down to 30 per cent and increase the 37 per cent threshold from $120,000 to $135,000.

(Source: Federal Government)

Additionally, the 45 per cent threshold is being increased from $180,000 to $190,000, and the lowest tax bracket drops to 16 per cent, from the current rate of 19 per cent, for those earning between $18,000 to $45,000.

Individuals earning above $120,000 will see the most substantial tax cuts due to the flattening of the tax brackets and the increase in the threshold for the highest tax rate.

The long political gestation of the tax reform culminated in the delivery of the cuts from Monday (1 July), after the Albanese government adjusted the original ruling Liberal Party’s measures to pare back benefits from the wealthy and bolster savings for low income earners.

Sally Tindall, Research Director, RateCity.com.au, said borrowers should start preparing their budgets for the possibility of not just one, but potentially two more rate hikes before the year’s end.

The tax cuts could both offset and contribute to this likelihood.

Source: RateCity.com.au. Notes: based on an owner-occupier paying principal and interest with 25 years remaining at the start of the hikes on the average variable rate back in April 2022 of 2.86%. Assumes cash rate increases are in August and November 2024 and that banks pass them on in full.

Ms Tindall said that for an owner-occupier with $500,000 debt at the start of the hikes and 25 years remaining, two more rate hikes would add another $150 onto their monthly mortgage repayments.

At existing interest rates, the cuts would still mean, for an average mortgage repayment of $3,681 a month on a $625,791 average loan, the tax cut could potentially wipe out one monthly mortgage repayment per year.

That is based on a dual income family with a combined household income of one person earning $100,000 and getting a $2,179 annual tax and another person earning $80,000 and getting a $1,679 tax cut.

The combined value of the tax cut in this case is $3,858.

As of 1 July, the national minimum wage was also increased by 3.75 per cent. The new rate will be $24.10 per hour.

Greater borrowing power

Helen Avis, Director of Finance, Specialist Mortgage, said the tax regime adjustment means many Australians will see an increase in their disposable income.

“Higher disposable income directly translates to enhanced borrowing capacity for prospective home owners and investors,” she said.

“These savings can significantly impact an individual’s serviceability for a mortgage, as lenders assess borrowing capacity based on net income.

“More take-home pay means borrowers can afford larger loans, leading to an uptick in borrowing power.”

To illustrate, Ms Avis noted that a single borrower earning $100,000 annually could see their borrowing capacity increase by approximately $50,000.

“This substantial boost could be the difference between securing a dream home and settling for a less desirable option,” she said.

Steve Douglas, Chairman, Australasian Taxation Services, said that the broader economic implications could amount to increased activity in the property market.

“The Stage 3 tax cuts are poised to stimulate the housing market by increasing demand through having 13.6 million Australians having some extra real income.”

“When individuals have more disposable income, they are more likely to invest in property, whether it be their first home, an upgrade, or an investment property.”

Mr Douglas highlighted the potential ripple effects on property prices.

“With increased borrowing capacity, we may see heightened competition in the housing market, which could drive property prices up.

Mortgage aggregator Aussie published on its website two examples of how the new tax changes could bolster borrowing power.

One such scenario indicated that single Australians with no dependents earning $120,000 per year in the financial year just concluded, who could borrow a maximum $615,135, will increase their borrowing capacity in Financial Year 2025 by $27,062 on a mortgage, based on a 6.28 per cent interest rate, to $642,197.

Additionally, a married couple with two dependents earning a combined taxable income of $280,000 will increase their borrowing capacity by $75,346 on a mortgage with a 6.28 per cent interest rate in FY25, which is a 5.64 per cent increase on their previous maximum borrowing amount of $1,334,871.

Inflation to May 2024 has taken a stunning turn, rising sharply and effectively quashing any hopes of an interest rate cut this year.

A shock rise in inflation for the year to May has extinguished any hope of an interest rate cut any time soon.

The monthly Consumer Price Index (CPI) indicator rose 4.0 per cent, up from 3.6 per cent in April, according to the latest data from the Australian Bureau of Statistics (ABS).

The figure is likely to send shockwaves through the corridors of the Reserve Bank of Australia’s Chifley Square offices in Sydney.

Michelle Marquardt, ABS head of prices statistics, offered some hope that the numbers were not as bad as they appear, although the RBA may see it differently.

“CPI inflation is often impacted by items with volatile price changes like automotive fuel, fruit and vegetables, and holiday travel.

“It can be helpful to exclude these items from the headline CPI to provide a view of underlying inflation, which was 4.0 per cent in May, down from 4.1 per cent in April.”

Wednesday’s Consumer Price Index (CPI) puts inflation well off the trajectory needed to return to the RBA’s target band of 2-3 per cent by the end of 2025.

Inflation has now risen from the 3.4 per cent recorded in December 2023 and January and February 2024, and if it carries through to the June quarter result to be released just before the August Reserve Bank Board meeting, it will put a cash rate increase well and truly on the agenda.

Canstar’s Group Executive, Financial Services, Steve Mickenbecker, said an interest rate rise was now possible, and perhaps soon.

“This increase in the CPI Indicator for May makes it the third on a trot, lifting from 3.4 percent in February to a staggering 4.0 percent for May, confirming that inflation is off the trajectory towards the 2 to 3 percent target band the RBA seeks.

“The increase in the CPI Indicator will have the Reserve Bank moving towards the starting blocks and readying to fire the interest rate increase gun, just as the men line up for the 100 metre final in Paris, presuming that June quarter inflation reflects the same trend.

“The CPI rose 1.0 percent in the March 2024 quarter from 0.6 percent in the December 2023 quarter and a further rise, or even a failure to fall, in the June quarter will test the Reserve Bank’s patience.

“With scant evidence that inflation is moving towards the target band, the Reserve Bank will feel uncomfortable waiting a further three months for the following release of quarterly CPI and will surely lift rates in August – the risk of baked-in inflationary expectations is too high,” Mr Mickenbecker said.

Renters, borrowers left to tackle inflation

It was a worrisome outlook for borrowers.

An increase of 0.25 percent would add another $100 to the monthly repayment on a $600,000 loan over 30 years.

Cruelly, the very people hardest hit by inflation will be the ones to pay the price if, as seems increasingly likely, the next interest rate move is upwards.

The most significant contributors to the annual rise to May was housing (5.2 per cent), up from 4.9 per cent in April. Rents increased 7.4 per cent for the year, reflecting a tight rental market across the country.

Increased loan repayments will hit borrowers, with rents also subsequently rising as landlords look to pass on at least some of their own elevated expenses.

Around a third of Australian households either rent (31.4 per cent) or were homeowners with mortgages (36.8 per cent). It is this cohort that will carry the load when it comes to tackling rising inflation.

Notes: based on an owner-occupier paying principal and interest with 25 years remaining at the start of the hikes on the average variable rate back in April 2022 of 2.86%. Assumes cash rate increases are in August and November 2024 and that banks pass them on in full. (Source: RateCity.com.au)

The stage three tax cuts that will kick in on 1 July are now being seen through a different lens too.

On the one hand, hopes they would help offset the rising cost of living are now being replaced by concerns they will only go towards higher mortgages and rents.

Just as disconcertingly, the tax cuts could have a further corrosive impact on inflation, ultimately delivering more pain than comfort.

The RBA does not meet until 6 August, giving it time to contemplate its next move with newer inflation data. On 18 June it kept interest rates on hold at 4.35 per cent.

Real Estate Institute of Australia President, Leanne Pilkington, said economic sluggishness should encourage the RBA to hold fire on interest rate increases.

“This stickiness in the final hurdle to beat inflation is the same as other countries are experiencing in getting inflation into the target range of their central banks.

“The CPI figures need to be taken against the background of an economy that is barely growing.

“While headline unemployment declined slightly in May, the trend unemployment rate rose a little from 3.9 per cent to 4 per cent, to its highest level since Covid lockdowns.

“GDP growth in the March quarter it was 0.1 per cent and 1.1 per cent for the year and trending down – on a per capita basis we have had four consecutive quarters of negative growth.

“The current uptick in inflation should not in itself flag an increase in interest rates but a delay in any drop,” Ms Pilkington said.

Building industry still struggling

The annual rise in new dwelling prices remained steady at 4.9 per cent, with builders passing on higher costs for labour and materials.

The ABS also released the March quarter engineering construction data on Wednesday (26 June) showing its first decline in two years.

The volume of engineering construction dropped by 2.3 per cent during the March 2024 quarter.

The reduction affected both public sector and private sector projects.

There was a 2.4 per cent fall in engineering construction work done for the public sector while the volume of private sector activity fell back by 2.2 per cent.

The reverse in engineering construction activity is ominous given that it was previously the main source of growth in the industry.

All three pillars of construction activity are now moving backwards.

Master Builders Australia CEO, Denita Wawn, said inflation was hurting construction too, and curtailing hopes of resolving the housing crisis.

“Inflation is a capacity killer, making investment more expensive and less attractive.

“On the ground, we continue to hear projects for new homes, commercial or infrastructure construction simply don’t stack up because it takes too long to build and is too costly.

“If we don’t get inflation under control and urgently start boosting housing supply we are in for a lengthy period of pain and depressed construction activity.

“We know governments have acknowledged that more reform is needed to reduce building costs but the rubber needs to hit the road.

“Bringing down housing and rental inflation can only be achieved once we get a move on and speed up planning reforms, address tradie shortages through domestic and skills migration pathways, reform the regulatory environment, and scrap damaging elements of recent IR changes,” Ms Wawn said.

The annual rise in new dwelling prices remained steady at 4.9 per cent, with builders passing on higher costs for labour and materials.

Article Q&A

What is the inflation rate in Australia?

The Australian Bureau of Statistics (ABS) has released the CPI Indicator for May 2024 showing an annual increase of 4.0 per cent. It has risen from the 3.4 per cent recorded in December 2023.

The Mortgage and Finance Association of Australia named Ms Avis Residential Finance Broker WA 2024, marking her second time atop this podium.

he mortgage and finance broking industry in Western Australia honoured this year’s achievers at the 2024 MFAA State Excellence Awards, with Helen Avis, Director of Finance, Specialist Mortgage, taking out one the most coveted awards for the second time.

The Mortgage and Finance Association of Australia named Ms Avis Residential Finance Broker WA 2024.

Ms Avis said the MFAA Excellence Awards are renowned for celebrating the highest standards of professionalism, integrity, and innovation in this finance field.

“This recognition is a significant milestone in my career, and I am deeply grateful for the acknowledgment of my hard work and dedication within the mortgage and finance industry,” Ms Avis said.

“Winning this award is not just a personal achievement but also a testament to the incredible team and clients I have had the privilege to work with.”

Ms Avis added that the award highlighted the significant contributions of women in the mortgage industry.

“It is a powerful reminder that with determination, passion, and the right support, we can achieve great heights.

“I hope this recognition inspires other women in our industry to pursue their goals with confidence and resilience.”

All Western Australia MFAA State Excellence Awards winners are finalists in their respective categories at the MFAA National Excellence Awards which will be held in Melbourne on Thursday 25 July following the MFAA National Conference.

Advice for borrowers struggling with deposit

While it’s often said a 20 per cent deposit is needed to qualify for a home loan, a significant number of borrowers are securing mortgages with smaller deposits, according to the latest data from APRA, the banking regulator.

Ms Avis said it was still possible to buy a property with a small deposit and could offer advice on structuring a loan application correctly.

In the March 2024 quarter, 31.0 per cent of new home loans (by value) had deposits of less than 20 per cent, while 6.2 per cent of new loans had deposits of less than 10 per cent.

“While more than three in 10 borrowers are taking out loans with deposits under 20 per cent, these figures are relatively low by historical standards.

“Back in December 2020, for example, 41.7 per cent of new loans had deposits of less than 20 per cent, while 11.3 per cent had deposits of less than 10 per cent.

“This illustrates how banks have tightened their lending standards, to ensure borrowers don’t take on an excessive amount of debt, yet it’s still possible to buy a property with a small deposit,” Ms Avis said.

Generally, these buyers will need to pay lender’s mortgage insurance (LMI) when purchasing a property with a deposit of less than 15-20 per cent.

Full list of MFAA winners

Residential Finance Broker Award

Helen Avis, Specialist Mortgage

Regional Finance Broker Award

Jasmine Bunter, Loan Market Geraldton

Business Development Manager Award – Aggregator

Renee Dewar, Loan Market

Business Development Manager Award – Lender/Support Service Provider

Petra Rebeira, Suncorp Bank

Commercial & Equipment Finance Broker Award

Steven McCaughey, Financewest Solutions

Community Champion Award

TAG Finance Australia

Customer Service Award – Business

Loan Market Ellenbrook

Customer Service Award – Individual

Nicole Williams, For Finance Sake

Diversified Business Award

TAG Finance Australia

Finance Broker Business Award

Loan Market Bal & Associates

Fintech Lender Award

ubank

Loan Administrator Award

Gracen Woodcock, Loan Market Geraldton

Major Lender Award

Macquarie Bank

Mutual/Credit Union Lender Award

P&N Bank

Newcomer Award

Kurtis Grace, Whiteroom Finance Goldfields

Non-Major Lender Award

Bankwest

Specialty Lender Award

Pepper Money

Young Professional Award

Robert Flynn, Vorteil Financial Group

Article Q&A

Can I buy property without a large deposit?

In the March 2024 quarter, 31.0 per cent of new home loans (by value) had deposits of less than 20 per cent, while 6.2 per cent of new loans had deposits of less than 10 per cent.

Your 2024 Comprehensive Guide to Off-the-Plan Finance for Australian Expatriates

Investing in off-the-plan properties can be an attractive option for Australian expatriates looking to secure a foothold in the Australian property market. However, navigating the finance landscape for such investments can be complex. Here’s what you need to know if you’re looking to invest in Australian Property as an Aussie expat and seeking finance for off-the-plan properties.

Understanding Off-the-Plan Finance for Australian properties

Off-the-plan finance refers to financing arrangements tailored specifically for properties that have yet to be constructed or completed. As an expatriate, it’s crucial to understand the unique financing challenges and opportunities associated with these types of investments.

Current Finance Landscape for Expatriates

In recent years, there have been significant changes in the finance landscape for Australian expatriates. Lenders have become more cautious due to regulatory changes and increased scrutiny on overseas income. Expats may encounter stricter lending criteria compared to resident borrowers.

Challenges Faced by Expatriate Borrowers

One of the main challenges faced by expatriate borrowers is proving income stability and affordability. Lenders may require additional documentation, such as employment contracts, tax returns, and bank statements, to verify income sources and assess repayment capacity. Moreover, fluctuations in foreign exchange rates can impact borrowing capacity and loan affordability.

Strategies to Overcome Financing Challenges

Aussie expatriates can employ various strategies, including:

Building a Strong Financial Profile

Maintaining a healthy credit history, saving for a larger deposit, and reducing debt can strengthen your financial profile and improve your chances of securing favourable financing terms.

Partnering with Specialist Mortgage Brokers

Engaging the services of experienced mortgage brokers who specialise in expatriate finance can provide invaluable support and access to a wide range of lenders. These brokers understand the unique needs of expatriate borrowers and can tailor solutions to suit individual circumstances.

Exploring Alternative Financing Options

Expatriates may explore alternative financing options, such as non-bank lenders or international banks with a presence in Australia. These institutions may offer more flexible lending criteria and competitive interest rates tailored to expatriate borrowers.

Seeking Professional Advice

Seeking advice from financial advisors, tax specialists, and legal professionals can help expatriates navigate the complexities of off-the-plan finance and ensure compliance with regulatory requirements.

Securing finance for off-the-plan properties as an Australian expatriate requires careful consideration of the current finance landscape, potential challenges, and available strategies. By staying informed, seeking expert advice, and partnering with specialist mortgage brokers, expatriates can overcome financing hurdles and successfully invest in off-the-plan properties in Australia.

Experts are divided on the likelihood of an RBA interest rate cut in the next few months, but all agree borrowers are banking on it.

With inflation figures having fallen to the lowest level in almost two years, even the prospect of a cash rate rise in 2024 is up for debate.

Mortgage broker Helen Avis (pictured above left), director of Specialist Mortgage, said her clients would breathe a sigh of relief if there were no further rate hikes over the next 12 months, with many feeling the pinch of the rising cost of living.

“Many buyers are concerned about the prospect of rate increases and their ability to service their mortgage,” Avis said.

“This is particularly evident within the first home buyer market who are often shopping at their maximum borrowing capacity, investors using property as collateral to secure finance, and our overseas clients who are often faced with higher rates than Australian residents.”

High hopes that interest rates won’t rise in first half

Avis said her clients are hopeful rates will remain on hold for the next six months, with most believing they won’t see rate cuts until 2025.

“Nearly all of our clients are choosing variable loans over fixed rates. This is in significate contrast to the height of the pandemic when borrowers were opting for low-rate fixed mortgages.”

Avis said clients’ sentiment towards the property market was still positive, “but they are approaching it with a little more caution”.

She said many clients were factoring in potential rate increases, often looking at property well under their maximum borrowing capacity.

Now is a great time for borrowers to take advantage of the competitive rate market.

“Our brokers are negotiating aggressively with our clients’ existing lenders to get the best variable rates, which is often preferable compared to switching to a new loan provider,” Avis said.

Buyers need to spend within means

aussieproperty.com buyers agent Julie Kelley said rate relief would instil confidence in the property market.

“As we all know taking on too much debt can lead to unnecessary stress; I always advise clients to shop in their comfort zone,” Kelley said.

“In such a competitive market, I understand buyers can feel frustrated by not being able to secure their dream home due to budget constraints, and they may feel pressured by selling agents to quickly submit an offer above their initial budget. But it’s important not to let emotions take over.

“We always advise our buyers that are considering pushing their borrowing limits to first speak with their mortgage broker and factor in all increased costs such as stamp duty, repayments and LMI before submitting an offer on a property”.

Financial comparison site Mozo’s money expert Rachel Wastell (pictured above centre), money expert at financial comparison site Mozo, said mortgage holders would welcome a rate cut, no matter how small.

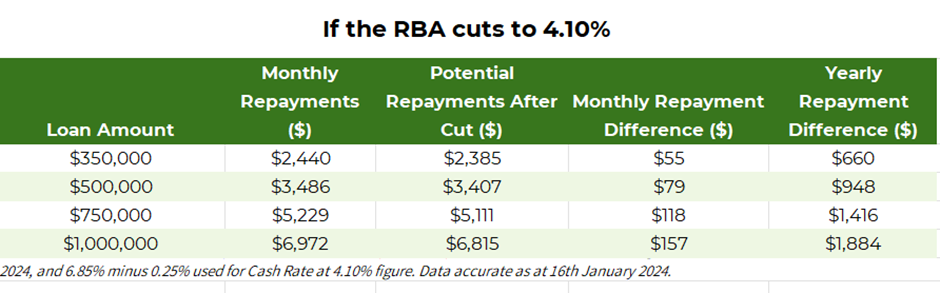

Mozo analysis shows someone with a $1 million mortgage, following a rate cut to 4.1%, will have an extra $157 a month in their pocket, equating to $1,884 a year based on the variable rate staying the same (see Mozo data below).

Source: Mozo

“I think borrowers will be cheering when a rate cut comes through,” Wastell said. “After one of the most aggressive rate hiking cycles since the early 1990s news about rates has unfortunately been quite doom and gloom.”

RBA on track to meet inflation goal?

Wastell said a rate cut will likely give borrowers some hope that the RBA is on track to meet their inflation target, and that more rate cuts could be on the horizon.

“In a cost-of-living crisis every cent counts; $100 more a month might not seem like much, but for those mortgage holders who have now resorted to credit cards or buy now pay later services to cover their everyday expenses,” Wastell said.

“That $100 could be the difference between clearing those monthly balances or being in the red.”

Despite what borrowers want, Wastell said a rate cut in the next few months was unlikely, as the unemployment rate was holding steady and inflation in services, particularly insurance, was still high.

“Later in the year, if there are no further rate hikes, and the CPI data for the June quarter shows we’re much closer to the RBA’s target of 2% to 3% we will probably see a rate cut or two, but I think it’s important homeowners don’t count their chickens before they hatch.”

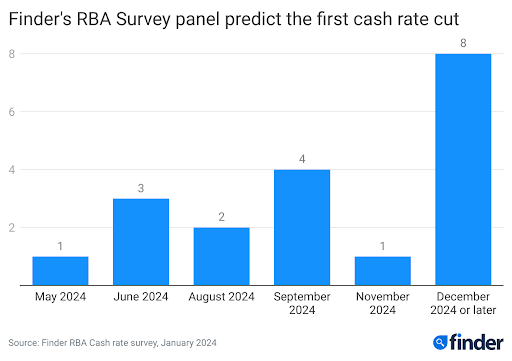

Experts predict February cash rate pause

In this month’s Finder RBA Cash Rate Survey, 19 experts and economists weighed in on future cash rate moves and almost all of the experts, 89%, said the RBA would hold the cash rate at 4.35% in February.

Head of consumer research at Finder Graham Cooke (pictured above right) said many Australians were in urgent need of reprieve following the last rate rise in November.

“Homeowners are still reeling from 13 rate hikes in the last two years,” Cooke said.

“Our data shows a staggering 40% struggled to pay their mortgage in December. Even though inflation is falling, I expect the RBA will hold the cash rate for most, if not all of 2024.”

While one in three Finder panellists predict a cash rate cut by at least August this year, almost half, or 40%, don’t expect the RBA to start cutting rates until December 2024 or later.

The majority of Finder experts, or 71%, said they expected the cost-of-living crisis to ease eventually in 2024.

“While the gauge remains in the extreme range, it’s likely that this will be where the cost-of-living pressure peaks,” Cooke said. “We expect to see some relief on the horizon, and with a little luck the pressure will reduce slowly over many months.”

Earlier this month, Bank of Queensland chief economist Peter Munckton said talk of rate increases by the RBA this year were “in the rear mirror” and said the big question for 2024 is when would interest rates start to fall.

Specialist Mortgage director Helen Avis settled more than $25 million in loans in July, as returning expats and those looking to move to lifestyle locations underpinned a record quarterly performance for mortgage brokers across the country.

Ms Avis completed 49 settlements collectively worth $25.03 million over the month, with that total eclipsing the next highest Australia-based Specialist Finance Group broker by more than $5 million.

Specialist Mortgage which operates in Sydney, Melbourne and Perth as well as international cities such as Singapore, Hong Kong, New York, Dubai and London aggregates to SFG.

The July total adds to a long list of achievements for Ms Avis, including winning St Georges Bank’s Top Flame Broker award in 2013 and 2014, and being named SFG’s International Broker of the year in 2016, 2017, 2018 and 2019.

Ms Avis said a big proportion of the July loans went to returning expats seeking a home in Australia to ride out the pandemic.

More than 500,000 Australians have returned from international cities since the onset of COVID-19, with that influx a big contributing factor to the meteoric rise in housing values over the past 12 months.

“The market is hugely competitive at the moment, and with the appeal of Australia being a safe haven from COVID-19, I’ve seen high demand for family homes being sought in Queensland and New South Wales,” Ms Avis said.

“Clients are looking at options for where to stay when they make it out of quarantine, and somewhere comfortable that they’ll be in for the future.”

One of those expats was Stewart Duncan, who heralded Ms Avis’ expertise in the complicated process of signing and notarising crucial documents for an offshore client.

“It was all a bit complex for a layman, but Helen navigated everything on my behalf and explained the pros and cons of different scenarios,” Mr Duncan said.

“I felt very comfortable being able to reach out to Helen at any time and get a quick response, especially not being in Australia with time differences and trying to get something in a timely manner.

“Doing business transactions is completely different to finding a house for the family and the support from having someone on the ground was immeasurable.”

Mr Duncan said he was extremely satisfied with the rates and the terms of the loan provided by Ms Avis.

“The process requires somebody familiar with the expatriate financial packages and terms and conditions to be able to explain them to the banks,” he said.

Another happy client was Peter, who recently returned to Australia from Singapore and purchased a family home on Sydney’s Lower North Shore and refinanced an investment property.

“We found dealing with Helen and her team a very positive experience,” Peter said.

“From quickly ascertaining our requirements and forwarding a number of attractive options from several lenders, we were able to work with Helen quickly from pre-approval to settlement.”

The strong monthly performance came in an environment of elevated demand for housing finance, with the value of new settlements in the second quarter of the year up 47.25 per cent compared to the same time in 2020.

Data released by the Mortgage & Finance Association of Australia showed there was more than $77.75 billion in new lending facilitated by brokers in the three months to the end of June, up $24.95 billion on the previous quarter.

The second quarter performance represented the biggest observed result for a June quarter and was $13.65 billion more than the previous record three month period since the MFAA commissioned CoreLogic to provide the data in 2013.

SMATS Group executive chairman Steve Douglas, who heads up the main holding entity of Specialist Mortgage, said 2021 had been one of the busiest he’d been involved in through his 25-plus years in migration and financial services.

“We are seeing more clients refinancing with these unprecedented low interest rates, and migrants wanting to return back to Australia are re-entering the property market to secure a property for their return,” Mr Douglas said.

“Given the relative safety from COVID-19 in Australia is it any wonder those Aussies living abroad are trying to get back?

“We’re not surprised, it’s certainly been keeping us busy.”